What if the greatest threat to a six-figure watch collection is not theft, but poor storage and inadequate insurance? In high-end horology, market value can be damaged as easily by humidity, handling errors, incomplete documentation, or a weak policy as by physical loss.

Collectors often focus on rarity, provenance, and condition at the moment of purchase, yet long-term value is preserved in the years that follow. Professional storage and specialized insurance turn passive ownership into active asset protection.

A fine watch is not merely a precision instrument or a personal indulgence; it is a portable store of capital in a market that rewards originality, traceability, and immaculate care. Even minor environmental damage or a disputed claim can materially weaken resale performance.

This is why serious collectors, family offices, and investors increasingly treat storage and insurance as part of valuation strategy itself. Protecting high-end horology means protecting the conditions, records, and legal safeguards that sustain its price in the market.

What Professional Watch Storage and Specialized Insurance Actually Protect in High-End Horology

What are you really protecting when you move a six-figure watch into professional storage and place it under a specialist policy? Not just theft risk. You are protecting originality, service traceability, cosmetic integrity, and the small documentation details that decide whether a piece trades as “collector-grade” or gets discounted hard.

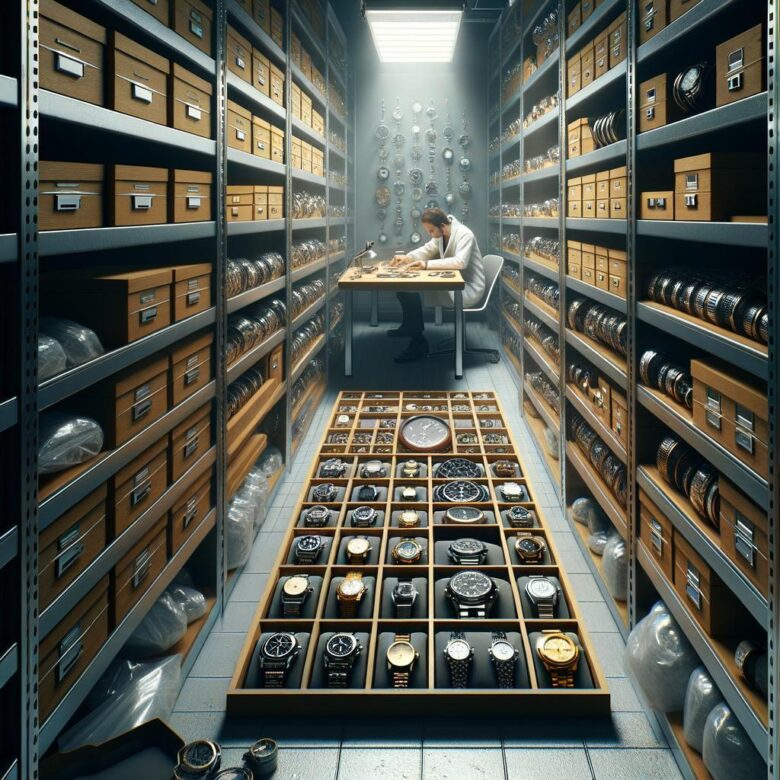

Professional storage is built around preservation risks that a home safe does not manage well: unstable humidity, magnetism from nearby electronics, gasket fatigue from poor sealing environments, accidental handling marks, and paperwork separation. In practice, facilities use controlled-access vaulting, environmental monitoring, intake photography, and chain-of-custody logs; platforms such as Crozier or specialist vault providers document condition in ways that become useful later in a claim or resale review.

Short version: condition drift matters.

- Storage protects physical marketability: dial lacquer, lume consistency, strap condition, box set completeness, and untouched case geometry.

- Insurance protects financial replacement complexity: agreed value, transit exposure, mysterious disappearance, and restoration after partial damage.

- Together they protect provenance: dated photos, service invoices, and movement/serial records that support authenticity disputes.

A real example: a collector stores a perpetual calendar in a standard safe with documents kept elsewhere. After a minor water ingress event during HVAC failure, the watch survives mechanically, but the stained warranty booklet and missing condition report create friction with both insurer and buyer. That is where specialist cover and professional intake records earn their keep.

One quick observation from the trade: buyers often forgive honest wear; they rarely forgive uncertainty. If storage and insurance cannot prove what happened, when, and in what condition, value erosion starts before damage is even confirmed.

How to Build a Secure Storage and Insurance Framework That Preserves Luxury Watch Market Value

Where does value actually get lost? Usually in the gap between “safe enough” storage and a framework that can survive a claim, a resale due-diligence review, or an insurer’s inspection. Build yours in layers: first a climate-stable primary location, then documented handling rules, then insurance terms matched to how the watch is really used.

Start with the storage environment, not the safe brochure. A heavy residential safe placed against an exterior wall or in a damp basement solves theft anxiety while quietly creating condensation risk; I have seen lacquered dials and leather straps suffer more from bad room placement than from wear. Keep the safe in an interior, temperature-stable room, use a calibrated hygrometer, and separate daily-wear pieces from long-term holdings so frequent access does not disturb every watch.

- Write a handling log: service dates, pressure-test results, strap changes, and who touched the watch.

- Photograph caseback, clasp, movement serial, accessories, and any existing marks; store the record in Google Drive and an offline encrypted copy.

- Schedule valuation reviews every 12 to 24 months, especially for independent brands and discontinued references.

A quick observation: many collectors insure the watch but not the evidence. That becomes a problem when a claim adjuster asks for proof of prior condition and completeness of set.

For insurance, avoid blanket assumptions. If a client rotates a Patek between home, office, and international travel, a standard homeowners rider often leaves dangerous gaps around mysterious disappearance, unattended vehicle storage, or territorial limits; specialist platforms such as Jewelers Mutual or brokers placing coverage through collectibles markets tend to be easier to align with real use. Ask one plain question-“Under what exact scenario would this claim be reduced?”-and get the answer in writing.

Common Storage, Documentation, and Coverage Mistakes That Quietly Erode Collectible Watch Resale Prices

Small mistakes compound. A watch can be mechanically perfect and still trade below market because the ownership trail looks careless. Creased warranty cards, water-stained manuals, a torn outer sleeve, or a replacement travel pouch where the original presentation box should be – buyers read those details as shortcuts, and dealers price in friction.

One pattern shows up often in private sales: the watch was stored in a safe, but the papers were kept in a separate drawer with household documents. A burst pipe, a move, or simple misfiling later, the set is no longer complete. I’ve seen modern Rolex and Patek listings lose negotiating power not because the watch had damage, but because the serial on the warranty document could not be matched quickly and confidently during due diligence.

- Leaving watches on constantly running winders that generate unnecessary wear on reversing wheels, rotor bearings, and calendar mechanisms.

- Storing boxes, tags, and booklets in attics, basements, or bank-safe packaging that traps moisture and encourages mildew or foxing.

- Failing to digitize provenance: service invoices, import papers, auction descriptions, and bracelet link counts should be logged in Chrono24 collections or a secure document vault like Dropbox.

And then there’s polishing. Yes, slightly adjacent, but it matters. Owners often keep service receipts yet forget to note when a case was refinished; later, a sharp-eyed buyer sees softened bevels and starts questioning everything else in the file.

The practical fix is boring but effective: keep the watch, accessories, and documentation cross-referenced with dated photos, serial captures, and service PDFs in one inventory workflow. If provenance takes ten minutes to prove instead of ten seconds, resale usually gets quieter – and cheaper.

Summary of Recommendations

Professional storage and insurance are not accessory services; they are part of the asset strategy for high-end horology. The right setup protects more than the watch itself-it preserves provenance, condition, and resale leverage when the market becomes selective. For collectors and investors, the practical decision is straightforward:

- use specialist storage when environmental control, security, or travel exposure create avoidable risk;

- review insurance terms with the same scrutiny applied to acquisition details;

- document every service, valuation, and movement of the piece.

In a market where small condition differences can move prices materially, disciplined protection is often what separates a merely expensive watch from a durable store of value.

Dr. Alistair Sterling is a leading economist and consultant specializing in alternative asset markets. With a PhD in Financial Economics, he has dedicated his career to analyzing the intersection of market volatility and tangible assets. As the founder of Bidphoria, Dr. Sterling provides collectors with the data-driven insights needed to transform passion into a sophisticated investment portfolio